Bitcoin crashed under $50,000 on August 5 in a sudden dip that noticed many positions liquidated within the crypto market. This sudden dip, which cascaded into different cryptocurrencies, took the market without warning. As such, Bitcoin fell to its lowest value in six months, and lots of different altcoins adopted swimsuit. Though Bitcoin has since recovered by 20% and now finds itself buying and selling round just under $60,000, many short-term holders are nonetheless sitting in unrealized losses.

A current report from Glassnode, a number one blockchain evaluation agency, sheds gentle on the elements contributing to this abrupt market downturn. The report means that the crash was largely pushed by an overreaction from short-term holders, who had been fast to liquidate their positions within the face of the preliminary decline.

Bitcoin Quick-Time period Holders Fast To Capitulate

Quick-term holders are usually outlined as these traders who maintain onto their cryptocurrency property for a comparatively temporary interval, typically round a month or so. As such, they’re rapidly liable to capitulating in periods of value corrections. This pattern has significantly been evident within the newest Bitcoin value correction/consolidation, which has lasted far longer than many traders anticipated.

Studying

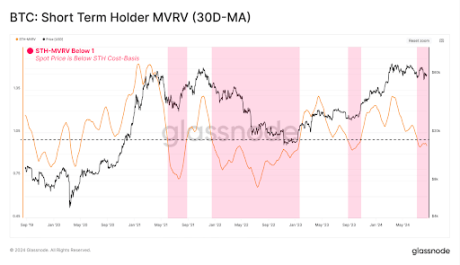

In line with Glassnode’s most up-to-date on-chain report, a key metric often called the STH-MVRV (Market Worth to Realized Worth) ratio has fallen under the crucial equilibrium worth of 1.0. When the STH-MVRV ratio dips under 1.0, it means that, on common, new traders are holding their Bitcoin at a loss relatively than a revenue. These unrealized losses, sometimes called paper losses, happen when the market worth of an asset is decrease than the worth at which it was acquired, however the asset has not but been bought. That is completely different from realized losses, which come up from accomplished trades.

Whereas intervals of temporary unrealized loss are widespread throughout bull markets, they have a tendency to place promoting strain on the worth of Bitcoin. It is because sustained intervals of STH-MVRV buying and selling under 1.0 typically result in a better probability of panic and capitulation amongst short-term holders. Notably, this phenomenon contributed to the Bitcoin crash earlier within the month.

Studying

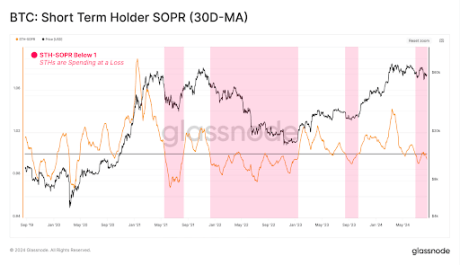

Moreover, Glassnode’s report reveals this correlation and promoting strain would possibly already be happening, with the STH-SOPR (Spent Output Revenue Ratio) additionally buying and selling under 1.0. The STH-SOPR ratio measures the profitability of spent outputs, indicating whether or not property are being bought at a revenue or loss. What this primarily means is that many short-term traders are extra taking realized losses than revenue. This follows the declare that many short-term holders have been overreacting to the worth corrections.

Whereas short-term holders have carried most of the losses throughout the current downturn, long-term holders stay sturdy. On the time of writing, Bitcoin is buying and selling at $59,540 and is down by 2.15% up to now 24 hours.

Featured picture created with Dall.E, chart from Tradingview.com