Is now a superb time to purchase a home?

It’s an evergreen query — at all times related — and it’s a extremely private query. Solely you possibly can reply whether or not or not it is sensible so that you can purchase a house at any given time.

That mentioned, the realities of unpredictable rates of interest and the ever altering housing market will play a job in your resolution. And, proper now, these indicators are blinking pink.

As of December 2022, shopper confidence is sort of low in accordance with Fannie Mae’s Home Purchase Sentiment Index. Solely 16% of shoppers imagine it’s at the moment a superb time to purchase a home. So who’s proper?

Is Now a Good Time to Purchase a Home?

As we method 2023, the dramatic improve in housing costs we have been seeing in 2021 has stalled. Actually, home prices have decreased for 9 consecutive months, in accordance with the Nationwide Affiliation of Realtors. Not solely that, however some consultants imagine the regular leak might change into a stream and a collapse in prices is coming.

On high of that, mounted 30-year mortgage rates of interest are hovering around 6.5% — as excessive as they’ve been in 20 years — although they did barely lower in November 2022.

When requested in regards to the outlook for mortgage charges in 2023, eight trade insiders advised Mortgage Reports they anticipated rates of interest to run wherever from 5% to 9% subsequent yr — fairly a variety that doesn’t essentially make a future homebuyer brim with pleasure.

Inflation might proceed to push charges up, whereas a looming recession would seemingly trigger them to drop. Ongoing inflation, Federal Reserve insurance policies and impending recession fears make the close to way forward for rates of interest tough to foretell.

That mentioned, should you’re set on shopping for a house quickly, you may have choices. You simply should be ready to tackle that monetary burden.

4 Inquiries to Take into account Earlier than You Purchase a Home

Finally, whether or not or not you can purchase a house proper now relies upon largely on how prepared you might be and your monetary scenario extra so than market situations.

Earlier than shopping for a house — the one largest buy most individuals will make — you could have a stable monetary plan in place. Listed below are some issues to think about earlier than making that buy.

1. How Lengthy Do You Count on to Keep in This House?

The longer term isn’t at all times predictable — life occurs in any case — however you must have an thought of any main selections which can be in your close to future.

Do you count on to get married? Do you propose on having youngsters within the subsequent 5 to 10 years? How everlasting is your present job scenario? Do you wish to be in that location long run?

If any of these conditions are in flux, you would possibly wish to pause shopping for a house proper now. That two-bedroom condominium would possibly get a little bit tight when you begin having youngsters. Or the home you thought was a dream might change into a monetary weight round your neck when your organization asks you to switch to a different metropolis.

The perfect time to purchase a home is when your life is pretty secure, each personally and professionally. That doesn’t imply you could have all the things completely set. However you must rigorously take into account the professionals of shopping for the house versus the cons of probably transferring within the quick time period — and determining what to do with your own home — due to life modifications.

2. How A lot of a Down Cost Can You Make?

Conventional knowledge has at all times mentioned to make a 20% down fee with the intention to keep away from non-public mortgage insurance coverage. PMI covers the lender in case you cease making funds.

The current median sales price for a house within the U.S. is $379,100. Which means to keep away from PMI, a purchaser would want to make a $75,820 down fee. For many consumers, that can require planning and a few aggressive financial savings earlier than making the acquisition.

The extra you set down, the much less your mortgage might be — that means decrease month-to-month funds. So you’ll borrow $303,280 as a substitute of a better quantity. Most lenders require a minimal down fee of round 3% to five%, so you may have that possibility in case your price range permits for bigger month-to-month funds (extra on that later).

First-time dwelling consumers usually have extra choices — with decrease down funds and credit score rating minimums. These embody:

- FHA Loans: In case you qualify, you would possibly take into account an FHA mortgage, insured by the Federal Housing Administration. These loans require simply 3.5% down and credit score rating minimal of 580. Or should you’re capable of put 10% down, you’ll solely want a 500 credit score rating.

- VA Loans: Veterans Affairs’ loans are an possibility for certified army members and veterans. They don’t require a down fee and normally include decrease rates of interest. They could require a funding payment that may be rolled into the general mortgage.

- USDA Loans: In case you’re seeking to reside in a rural space, it’s possible you’ll qualify for a mortgage from the U.S. Division of Agriculture. These loans require no down fee. You’ll must reside in a qualifying space although.

Keep in mind, the extra you possibly can handle to place down on the entrance finish, the much less debt you’ll carry over the course of your mortgage.

3. What About Your Credit score Rating?

Be sure to know your credit score rating properly earlier than you start the method of shopping for a house. That one little quantity will tremendously have an effect on your mortgage choices when it comes time to signal the mortgage.

The usual magic quantity required for typical loans is 620. Something between 670-739 is taken into account “good.” Between 740-799 is taken into account “superb.” And something above 800 means you may have “wonderful” credit score. The higher your credit score rating, the higher your mortgage choices and rates of interest might be.

Non-conventional loans would require increased credit score scores. One instance is a jumbo mortgage, which usually requires a credit score rating of round 700. There are methods to purchase a home with a decrease credit score rating although.

In case you’re looking to buy a house within the close to future, it’s extremely essential to be sure you perceive the place your credit score rating is and how one can enhance it over time.

There are many methods you possibly can actively work on enhancing your credit score rating — all the things from making on time funds, making use of for credit score selectively and even asking for a credit score restrict improve however not utilizing it.

4. Is Your Price range Prepared?

The median mortgage fee is $1,100, in accordance with American Housing Survey data. That quantity can range, in fact, based mostly on the place you reside, how lengthy your mortgage is, your down fee and rate of interest.

But when solely that was all you have been anticipated to pay. It’s simple to overlook all the opposite charges that get tacked on to mortgage funds. You’ve received taxes, insurance coverage and possibly HOA charges and mortgage insurance coverage — after which there’s all the continued upkeep and different month-to-month bills that include proudly owning a house.

Methods to See If You Can Afford a Home

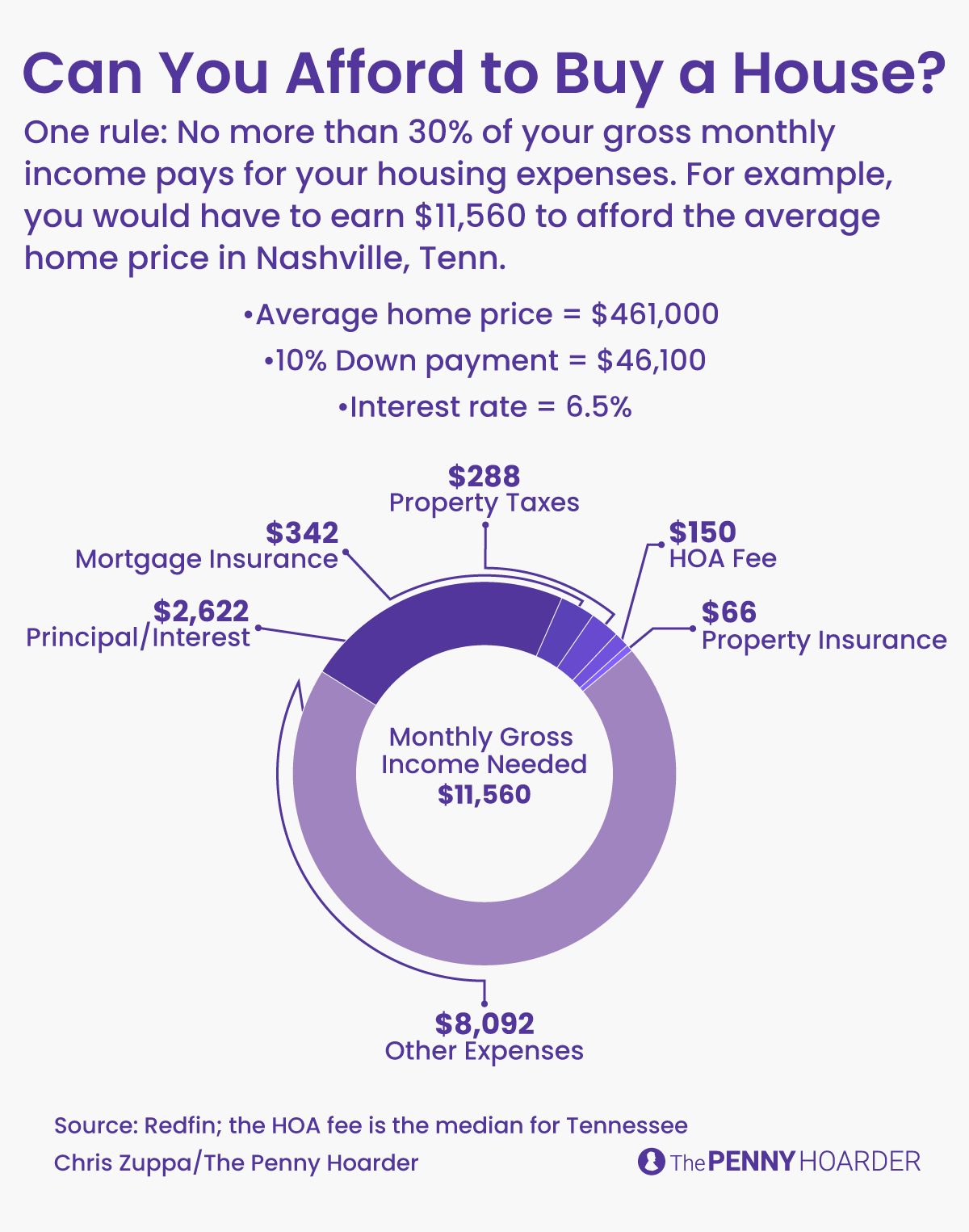

Let’s use an instance. We’ll say you reside in Nashville, Tennessee — a prospering actual property market, however not uncontrolled. As of now, the average cost of a home in Nashville is $461,000.

We’ll additionally say you reside in a home-owner’s affiliation — and, happily sufficient for you, Tennessee has the fifth lowest HOA with a median of $150 monthly.

We’ll assume you may have good credit score and may get the common rate of interest proper now at 6.5%.

And we’ll lastly assume you possibly can handle a ten% down fee on a 30-year mortgage.

Final, that credit score rating can also be ok to get a good PMI fee of about 0.99%.

Let’s run the numbers.

- The mortgage fee: A $461,000 buy value with a ten% down fee ($46,100) brings you to a $400,000 mortgage. Together with principal and curiosity, that involves a $2,622 month-to-month fee. However that’s only the start.

- The taxes: Your Nashville zip code — and its corresponding property tax — will price you about $288 monthly.

- The insurance coverage: Home-owner’s insurance coverage runs about $66 monthly.

- The HOA charges: And we’ll tack on the median Tennessee HOA month-to-month fee of $150.

- The PMI: Then there’s PMI, which you’ll must pay because you’re making a down fee of lower than 20%. Your PMI fee of 0.99% involves a $4,104 annual premium, or $342 monthly. Remember, when you attain that 20% fairness quantity, you’ll not must make this fee. In case you made this normal fee each month, by no means paying additional, that may take slightly below eight years.

So, all mentioned, you’re truly paying $3,468 a month to your $400,000 mortgage — $846 of which is just added on after principal and curiosity.

The query is, potential Nashville house owner, do you may have $3,468 of flexibility in your present price range? (Remember that you’ll need to pay for upkeep and repairs too on high of that.)

If not, proper now might be not one of the best time to purchase a home.

It goes with out saying, though we at the moment are saying it, that your numbers might range tremendously the place you reside. A house in New York or San Francisco will price a lot a couple of in Nashville, whereas a house within the rural Midwest would price a lot much less. (A Midwest state would possibly even pay you to maneuver there.) Property taxes and HOA charges also can range tremendously based mostly on the place you reside.

The purpose of this train is to indicate how you could know precisely what you might be entering into earlier than leaping into a large buy like a house.

However What About Curiosity Charges?

All that to say what’s true now won’t be true 5 years from now, and even subsequent yr. As we method the tip of 2022, interest rates on a 30-year mortgage are pushing 7%. In 2015, they hovered between 3% and 4%. And originally of 2021, they have been as little as 2.7%.

In case you’re set on shopping for a home proper now, even with the upper rates of interest, you possibly can at all times refinance as soon as charges drop – and historical past tells us they most actually will drop.

For our $400,000 instance, you’ll pay round $800 extra monthly with a 6.8% rate of interest over a 3.8% fee. That’s an enormous distinction, and it’s one thing to bear in mind as you’re figuring out if now’s the fitting time.

So Is It a Good Time to Purchase a Home?

Primarily based on what many consultants are saying, in addition to how most people feels in regards to the housing market, it’s in all probability not one of the best time to purchase. We’re positively in a vendor’s market proper now.

However as you’ve seen, loads of variables are at play in how one can make that call. Most consumers proper now aren’t comfy as dwelling values and rates of interest are so excessive. However your scenario could also be totally different.

House costs are at all times altering. Rates of interest are at all times adjusting. What we’ll see this time subsequent yr might be drastically totally different from what we’re seeing now.

Know your price range. Know your credit score rating. Perceive how a lot of a down fee you may make, and the impression it is going to have in your month-to-month fee. And easily be reasonable about your present life scenario and the way that would impression the place you reside within the close to future.

Robert Bruce is a senior author for The PNW.